The Retirement Newsletter: Money — how much do I need to retire?

Issue Number: -127 — how much do I need?

Photo by Zac Durant on Unsplash

Welcome

Last week (Issue: -128 — When should I retire?) I wrote about how I came up with my retirement date. As I said in that issue, there are several ways you can come up with a date, one of which is money, and in this issue, we will start to look at money.

Money

OK, first off, I am not a financial advisor. I am writing about what I have read over the years about money and preparing to retire. This is not financial advice.

How much do you need to retire?

An interesting question?

Well, we need to establish how much money you need per year, and this can be determined by the level of retirement you desire which can be viewed as follows:

Essential — what is the minimum amount you need to survive? To live? To get by? Admittedly, not the most comfortable way to be retired, but you can at least be retired and have some freedom, albeit limited by money. Being retired at this level can be tough and you might have to top up your pension income with a part-time job.

Moderate — a comfortable retirement. A retirement where you are not overly limited by money. A retirement where you can travel and do things you want to do.

Luxury — a retirement where money isn't a serious concern. You can't go mad, but you can afford some nice holidays and have a very comfortable lifestyle.

Which one do you want? And is there a fourth level?

Be happy!

Well, I recently came across an article in the BBC Science Focus Magazine (yes, I read some odd stuff — and sorry, no link, it is behind a paywall) — How Much Money Do You Need To Be Happy? — and it suggested you need £33,864 (USD approx. $50,000) per year to be happy. To me, this figure seemed to be a little high, particularly for a retired person, so I did a little digging.

So, what did I find?

The article in the BBC Science Focus Magazine didn't have any references for how the sum of £33,864 was derived or what expenses were included in the figure. For example, did the figure include a mortgage, was it for a family or a single person? Basically, a poorly researched article. All the piece said was:

"In 2020, researchers analysed data from the Office for National Statistics and Happy Planet Index to find out how much money the average Briton would need to live a happy life."

What researchers?

After some quick Google searches, I think I tracked down the source of the information — raisin — who published an article — Does money buy happiness? Find out how much money you need to be happy around the world — in which they have taken data from the Office for National Statistics (ONS) in the UK and data from the Happy Planet Index to come up with figure.

Essentially, they used the data to identify the top 20 'happy' cities and towns in the UK and worked out the average income for those places — £33,864. Not exactly super robust science.

And, if £33,864 is correct — and I doubt it is, then how much do we need in our pension pot to retire and be happy?

Maths — how much?

Well, as it turns out, the maths is pretty simple to work out how much you need in your pot. You take the amount of money you think you will need per year and multiply it by the number of years you will be retired while factoring in inflation.

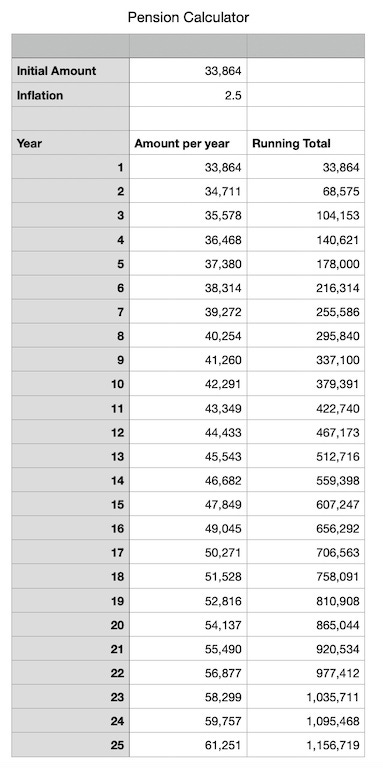

So, let's assume we do need £33,864 per year to be happy, inflation is running at 2.5% per year, and you think you will, and let's be blunt about this, live 25 years after you retire.

Now, the inflation rate is compound; that is, in the second year, you need to increase the amount you will spend by 2.5%, but in the third year, it is the initial amount, plus the first 2.5%, with 2.5% added. It doesn't sound straightforward, but it is easy to calculate using a spreadsheet.

And, as you can see, in year 25, you would need £61,251 per year to maintain your spending power (and be happy) and a total starting pension pot of £1,156,719. That is a lot of money!

Yet, you need more than that as you have to factor in tax. The £1,156,719 is post-tax, and as we will see in later newsletters, factoring in tax can be tricky.

Furthermore, the above doesn't consider any interest you are making on your pension pot, but it does focus the mind.

Summary

OK, so we have looked at a simple pension plan — the Be Happy Plan, and as you can see, you need a large pension pot. But, things may not be as bad as they seem, and there will be more on that in later newsletters.

Please note I am not a financial advisor. I am writing about what I have read over the years about money and preparing to retire. This is not financial advice.

In the news

I can't make up my mind if this is a good thing or a bad thing:

Artificial Intelligence may diagnose dementia in a day — BBC

Nostalgia corner

This past week, I have been attending a major international sporting event. It is an event I have attended pretty much every year (except for two when I was working overseas) since I was six months old.

When I went to the event as a child, it was a big family gathering. I had my parents there, grandparents, aunts and uncles, and my cousins. These days, the 'family crowd' is diminished with just a couple of family members, but going to the event brings back many memories and allows for the formation of new ones.

Stepping back and keeping traditions going is not a bad thing.

Useful links

UK Government Website — How to avoid pension scams

Next week

Next week I will look at retirement in a bit more detail, and the week after, I will return to money and start to explore beyond the 'be happy' plan.

Thanks

Thanks for taking the time to read this newsletter, and please don't hesitate to share it with your friends or on social media using the buttons below.

If you would like to say 'thanks for the letter, and you are not a subscriber, then why not buy me a cup of tea?

Until next time,

Nick

PS, If you have something you would like to contribute to the newsletter — a story, advice, anything — please get in touch.

Please note: I am not a financial advisor. When I am writing about money and financial matters, it is based on things I have read about money and about preparing to retire. THIS IS NOT FINANCIAL ADVICE.